Mortgage Servicing Ratio - MSR

Having a place to call our own is a crucial milestone in adulthood. Purchasing a home, which ranks among the largest investments we make, demands careful financial planning.

How can we effectively manage our finances to ensure we don’t exceed our means? One approach is to employ housing ratios, which reveal the portion of our income dedicated to housing expenses. By comprehending these ratios, we gain a better understanding of our financial capacity for housing requirements. Below are two helpful ratios that assist in maintaining a balanced housing budget

What is MSR?

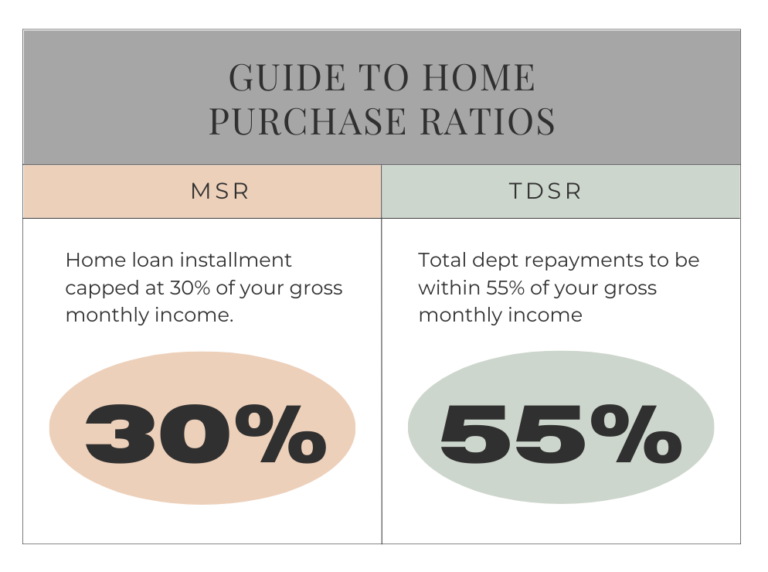

When buying a property in Singapore, you might be familiar with the TDSR, which limits debt repayments to 55% of a borrower’s gross monthly income. However, the MSR for HDB flats is equally important for loan qualification. The MSR specifically applies to HDB flats and ECs purchased from developers.

All HDB-issued loans and loans issued by banks for both HDB flats and ECs have an MSR of 30%. It sets a maximum limit of 30% of a borrower’s gross monthly income that can be used for mortgage repayments. For example, if you earn $5,000 per month, your monthly home loan installments cannot exceed $1,500.

Calculating MSR

To calculate the MSR, divide a borrower’s monthly mortgage obligations (including property-secured debts) by their total gross monthly income. For joint borrowers, divide their total monthly mortgage obligations by their combined gross monthly income. The formula for MSR calculation is:

(Monthly repayment installments for all property loans / Gross monthly income) x 100% = MSR (which has to be less than 30%)

MSR Calculator

PropertyGuru offers a convenient MSR calculator. Click here to check your MSR

What is TDSR?

You should be aware of the Total Debt Servicing Ratio (TDSR), which determines the highest percentage of your total monthly income that can be used to repay all your monthly debt obligations. This measure is in place to ensure that you don’t become overwhelmed in managing your debt.

Keep in mind that debt obligations include various types of loans such as those related to properties, including the loan you are currently applying for, auto loans, student loans, renovation loans, credit card loans, and any other secured or unsecured loans, like revolving loans.

As of 16th December 2021, the TDSR has a maximum limit of 55% of your gross monthly income. It is important to note that this limit specifically applies to property loans offered by financial institutions. However, loans obtained from the Housing Development Board (HDB) are not subject to the TDSR rules.

To calculate your TDSR, you can use the following formula: